Effective March 1, the SBA no longer requires a minimum FICO SBSS score to obtain an SBA loan.

What does this mean for you?

As of June 2025, the SBSS minimum score for SBA loan applicants was 165, automatically disqualifying entrepreneurs whose scores were lower.

![]() SBSS incorporates personal credit history of owners, business credit history, time in business, annual revenue, cash flow and bank balances, public records, industry risk profiles, trade lines and payment history.

SBSS incorporates personal credit history of owners, business credit history, time in business, annual revenue, cash flow and bank balances, public records, industry risk profiles, trade lines and payment history.

For many prospective borrowers, the rolling back of a mandatory SBSS minimum means the path to loan approval may have just opened up, especially for businesses that have struggled in any one of the aforementioned areas.

How your SBSS affects your loan approval will ultimately be at the discretion of individual lenders, some of whom may choose to place more weight on factors other than credit scores.

For small business owners with low credit but strong cash flow or collateral, this changes the game.

This is also helpful for younger businesses with a shorter credit history, especially if that business is generating strong, consistent revenue.

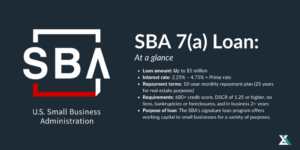

Interested in applying for an SBA 7(a) loan?

Interested in applying for an SBA 7(a) loan?

Apply today in just 10 minutes with no commitment and no credit impact.