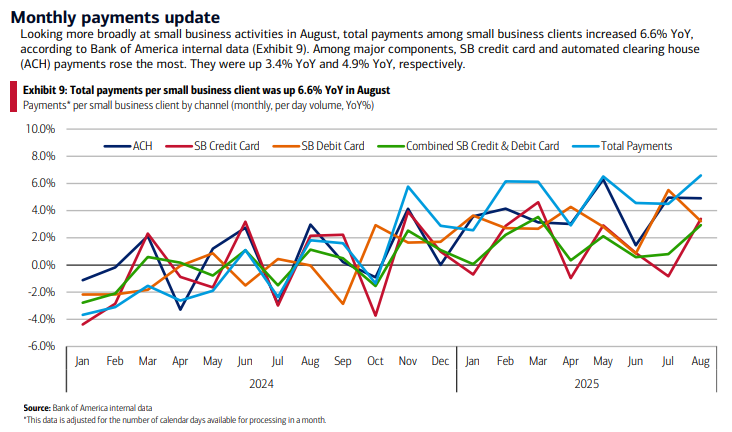

What the Data Shows Bank of America tracks small business automated clearing house (ACH) payments to lenders, a measure of how much businesses are sending each month to service their loan obligations. Interestingly, this dataset excludes Bank of America’s own loans and credit lines, offering a broader view of the market. This payments data is valuable because it reflects actual cash flow behavior rather than survey responses or sentiment. Rising payments indicate that more small businesses are borrowing and actively servicing debt. In last week’s Bank of America Institute’s Small Business Checkpoint report, data shows a modest but steady increase in small business payments to lenders. This trend suggests that financing activity is picking up, even though survey data from the NFIB indicates that only 23% of small business owners report borrowing on a regular basis. Why This Matters High interest rates often place pressure on businesses with variable-rate loans, as debt service costs rise alongside rates. However, with the Federal Reserve’s short-term rate easing slightly from last year, small businesses appear more willing to take on financing again. The increase in payments to lenders implies that the recent slowdown in borrowing was driven not only by tighter bank policies but also by reduced borrower demand. On the supply side, the Federal Reserve’s Senior Loan Officer Opinion Survey (SLOOS) indicates that banks have continued to tighten commercial and industrial (C&I) lending standards for small firms in 2025. Even so, the degree of tightening remains lower for small businesses than for large firms. This suggests that while credit availability is somewhat constrained, cautious borrower sentiment is playing an equally important role. Capital Spending and Selectivity Bank of America data also shows that small businesses maintained spending on technology services in August, underscoring a focus on productivity and long-term growth. At the same time, businesses reduced discretionary spending, particularly in categories such as travel. This indicates a selective approach to capital allocation, with investment directed toward areas most likely to enhance efficiency. The Bottom Line Banks remain cautious in extending credit, but business owners themselves are demonstrating restraint in how much debt they are willing to assume. As interest rates ease and uncertainty diminishes, borrowing activity and lender payments are expected to gradually improve. |